For many years, growth and consolidation have been key themes in U.S. healthcare. From hospital systems and insurance providers to independent practices and specialty clinics, every sector of the healthcare market has seen significant investment and buyouts. Prior to 2020, private equity was primarily focused on specialty providers in fields such as urology, ophthalmology, and dermatology. Recently, however, there has been a growing interest in other physician practice management (PPM) specialties – particularly those with current or future potential within the value-based care environment. As a result, pediatric primary care, a space historically insulated from the interest of institutional investors, is now attracting a notable share of private equity attention.

The allure of pediatrics for private equity investors stems from several factors: overarching macroeconomic shifts toward managed care, the consistent flow of patient visits, burgeoning market segments such as Pediatric Behavioral Health, Urgent Care, and Clinical Research, among others, and the potential to enhance value propositions and create economies of scale. Additionally, many private equity investors, having found success in specialty provider fields, are now seeking new, emerging healthcare sectors where they can create value. As the payor environment shifts toward quality care, opportunities to leverage scale and generate value are becoming more apparent, prompting investors to explore the pediatric market.

Trend 1 – Payor Dynamics

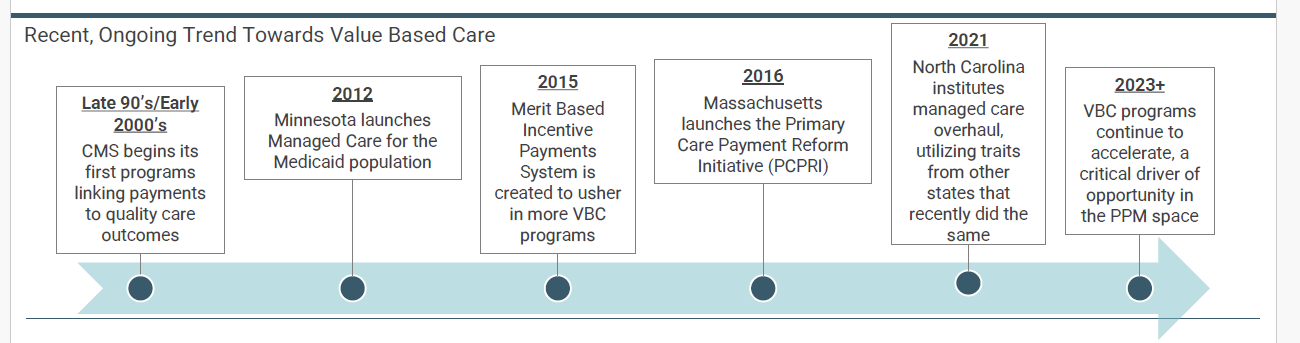

Payor dynamics are evolving rapidly, making primary care and pediatric care focal points for private equity investments in the physician practice management (PPM) space. The shift from fee-for-service to managed care / value-based models started in the late 90’s when programs began to link payments to quality-of-care outcomes. Over the past couple decades, more and more states have found ways to create savings through incentivizing quality care and rewarding providers by passing on savings through VBC programs or incentive payments. The trend towards quality care and valued based care has prompted practices to reevaluate their operations, making them attractive targets for private equity.

Trend 2 – Value Based Care & Aligning Incentives

Private Equity is drawn to the opportunity to allow physicians to maintain self-governance, while investors aim to reap the benefits of a value-based environment that rewards scale and controlling quality across a large patient population. Platforms can create value with scale through the establishment or broadening of shared Savings contracts, monthly revenue from managed lives (capitation), and quality incentive bonus programs. Additionally, investors are seeing opportunities to expand into adjacent pediatric specialties like behavioral health, urgent care, clinical research, allergy, dermatology, and other tangential areas of medicine.

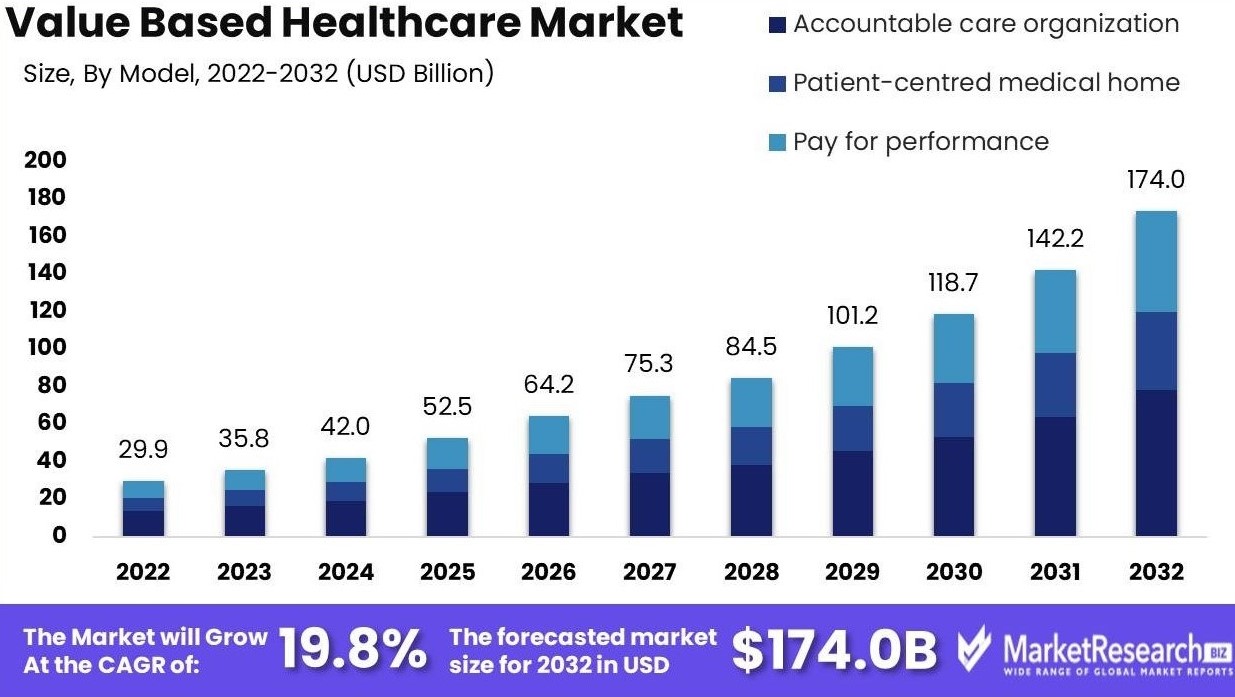

Source: MarketResearch Biz

Pediatrics is in the very early stages of its consolidation journey and is expected to accelerate greatly over the next five years. With over 60,000 active pediatric physicians in the United States, a significant portion of these smaller groups consists of less than five providers.1

While pediatrics is a relatively new area of interest for private equity with two traditional platforms established thus far, two other strategic alternatives exist, with Aspen Pediatrics (The Nashton Company) and Pediatrix (NYSE: MD). Notably, In Q1 2023, Webster Equity Partners, recognized for their extensive experience in physician practice investments, joined forces with Pediatric Affiliates in New Jersey, to form US Pediatric Partners. Physician Growth Partners served as the exclusive transaction advisor to the founding practice, Pediatric Affiliates. Since Webster’s initial investment in New Jersey, they’ve grown their footprint in the state while expanding to New York, South Carolina, and North Carolina. In addition, Summit Partners-backed Pediatric Associates started with their initial practice in Florida and has expanded in recent years to additional states such as California, Pennsylvania, New York, and New Jersey.

Given private equity’s growing interest in the pediatric vertical, there is an opportunity for groups to partner with private equity sponsors to establish their own platform as an “early mover,” or to align with an existing strategic partner in the early stages of its life cycle. The intersection of consolidation and widespread overhaul of reimbursement dynamics in the U.S. has created a particularly appealing opportunity for pediatric physicians, who have experienced the headwinds of independent medicine exponentially and acutely compared to provider peers in other verticals.

At PGP, we have experienced a surge of inbound discussions with pediatric groups across the country trying to navigate the landscape. And on the other side, more and more private equity firms who have yet to invest in pediatrics have expressed interest. As such, we expect deal activity to heat up going into the second half of 2024 and into 2025, and it is imperative pediatric physician groups keep a few key considerations in mind.

When evaluating a potential partner, it is extremely important to find the right fit to ensure a strong go-forward partnership. PGP advises that four critical factors need to be considered when evaluating whether a partner is right for your practice

While many independent groups may initially feel they can navigate a transaction without an advisor, those that have gone through the process with an experienced and reputable firm in their corner will be quick to highlight the significant value add from both economic, partnership and educational perspectives. Ensuring that each shareholder is prepared and fully understands the dynamics within a transaction is crucial for the future success of the business.

A seasoned healthcare transaction advisory team can ensure that the most attractive outcome is achieved. Through a formalized competitive marketing process, an advisor can ensure the practice maximizes their economics and transaction terms. A transaction process also allows the practice to interview multiple private equity partners and choose the group that presents the best ‘fit’.

Even if a group is approached by a buyer or has a buyer in mind, it is essential to run a process considering the practice has one opportunity to choose the right private equity partner, supplemented by the value a process drives regarding both deal terms and economics.

One of the biggest questions practice owners have is what happens after the transaction is consummated? In reality, if you are doing a transaction with a reputable private equity platform, physicians will largely continue to operate “business as usual”. The private equity partner will look to implement certain growth initiatives, but these initiatives will all be items that were discussed at great length in advance of consummating the transaction. On the clinical front, physicians will practice medicine the way they always have. Clinical autonomy is maintained, and an advisory firm like PGP negotiates this on the physician group’s behalf. As for infrastructure capabilities, groups that lack back-office sophistication will typically integrate into the “platform” practices EMR, Accounting and PM systems. Outside of day-to-day operations and clinical delivery, the most notable change is the holding of rollover equity in the new partnership by selling physicians. Due to the fact a substantial liquidity event is experienced, shareholders are required to utilize a percentage of their proceeds in the form of equity in the new enterprise. This is desired by the private equity firms as they want to maintain alignment with the physicians that they have invested in, creating a shared goal of a “second bite of the apple” when the platform ultimately experiences a subsequent sale 3–7 years down the road.

Gaining Payer

Leverage

Capturing In-House

Ancillary Services

Centralizing Infrastructure

and Operations

Resulting In

Sustaining Organic Growth

The consolidation within pediatrics continues to accelerate into the second half of 2024 and PGP expects the pace to continue into 2025. Whether a practice outwardly desires private equity partnership, questions the rationale and effectiveness of a PE partner, or downright disagrees with private equity, it is essential to get educated and ensure your practice is positioned for continued success in your market.

For those that choose to go down the path, it is imperative that culture and alignment, not simply economics, is the first goal. The role of an advisor like PGP can be the difference maker not only in knowing who can be trusted and who has a track record of success, but in ensuring an economic outcome that is satisfactory when transferring the ownership of your business.

If interested in pursuing a transaction, learning about private equity, the private equity strategy, transaction dynamics, or activity in your market, please utilize the information below to contact the PGP team and schedule a discussion.

1 Definitive Healthcare