Ambulatory surgery centers (“ASCs”) remain one of the fastest growing sectors of U.S. healthcare delivery. Driven by a decided shift to outpatient settings, appetite for physician alignment, and patient demand for convenient, lower-cost surgical settings, the number of Medicare-certified ASCs has steadily increased from just over 5,200 in 2011 to nearly 6,400 by 2024.1

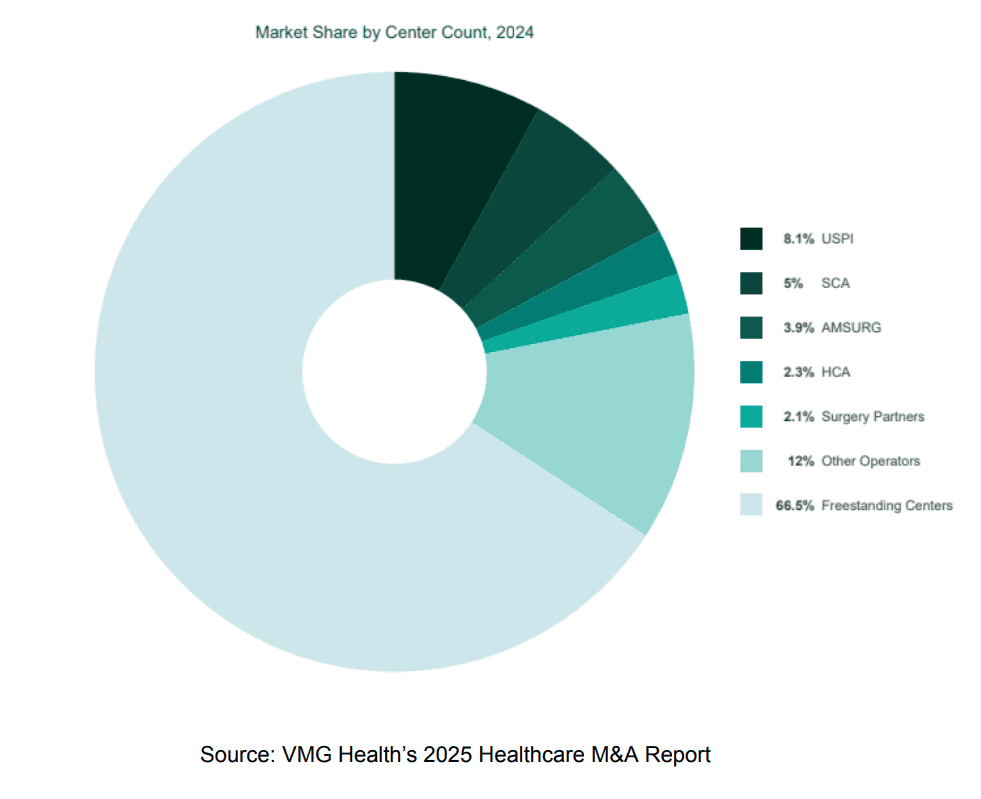

Despite this growth, the market remains highly fragmented, with approximately 67% of freestanding ASCs still independently owned and operated, as evidenced by VMG Health’s 2025 Healthcare M&A Report (pie chart below). The remaining facilities are concentrated among national operators such as USPI (owned by Tenet Healthcare), SCA Health (owned by Optum/UnitedHealth), AMSURG, HCA, Surgery Partners, and other operators. This fragmentation, coupled with steady case migration from hospitals to outpatient centers, makes ASCs a focal point for investment.

Consolidation in the ASC space is being driven by a broad set of buyers, including private equity investors, ASC management companies, and health systems. As of August 2025, there are more than 18 national ASC acquirers and many more significant footprints in regional markets. Private equity sponsors have been active in building multispecialty ASC platforms, as well as specialty platforms with an ASC component to capture surgery-related patient demand. At the same time, large operators such as Surgery Partners, the only standalone public ASC company, and the ASC divisions of Tenet, UnitedHealth, HCA, and other health systems are actively pursuing joint ventures to continue expanding their networks. Buyers are attracted to the consistent cash flow, growth potential, and alignment of physician ownership and incentives that ASCs offer.

Source: Ambulatory Surgery Center Association, March 2025

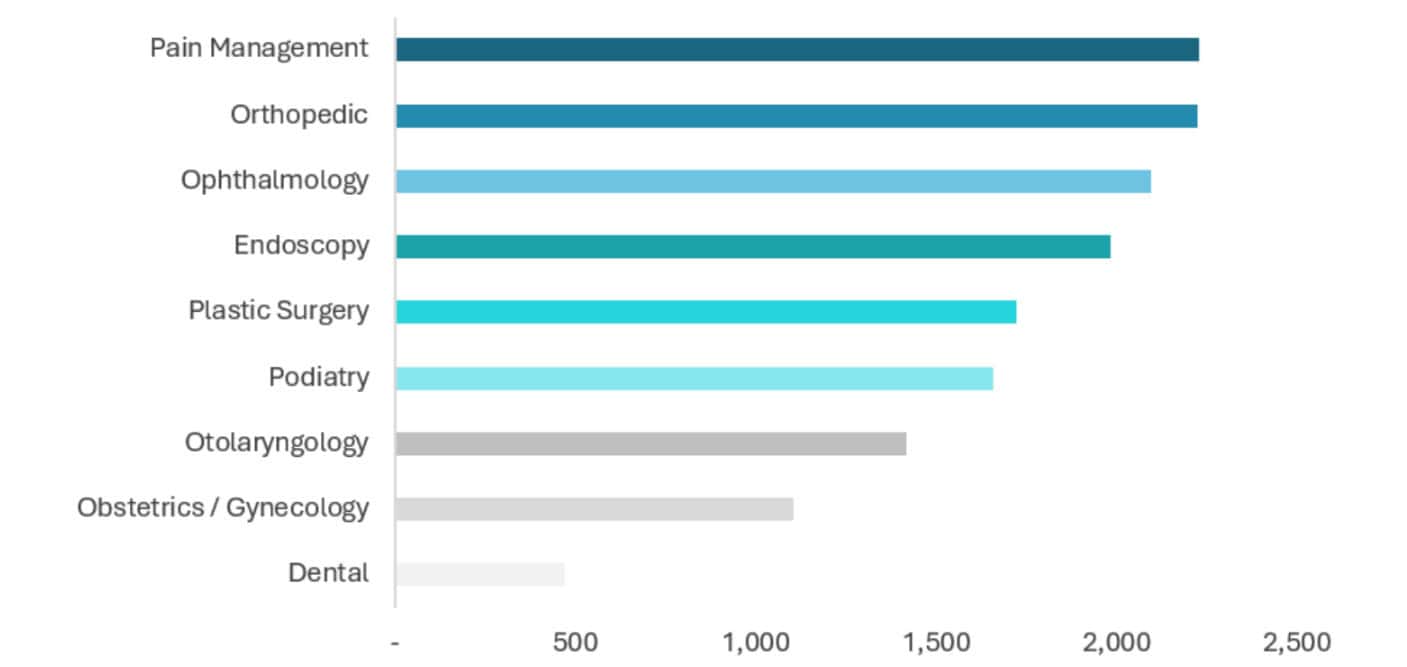

Patient volume across numerous specialties has continued migrating to the outpatient care setting, with the most prominent types being pain management and orthopedic, ophthalmology, and endoscopy / gastroenterology.2 Both single- and multi-specialty strategies are taking shape across the country as patients, providers, and payors favor the lower cost, more convenient services offered by ASCs.

When it comes to exploring a sale, it is imperative that ASC owners engage a professional advisory team, which typically includes a healthcare services-focused investment banking team like Physician Growth Partners (“PGP”) and a legal advisor, who act as an extension of the shareholders and leadership team.

Our experienced team at PGP has successfully guided several ASCs through the transaction process. There are several steps that we take to ensure successful outcomes for our clients, including but not limited to:

12025 Healthcare M&A Report – VMG Health

2Ambulatory Surgery Center Association. Note: ASCs with more than one specialty are included in each specialty type that they offer

Introduction Ambulatory Surgery Centers remain one of the strongest corners of healthcare services M&A. Investment has compounded over the last decade as payers, providers, and patients push procedures to lower-cost...